企业区位视角下的数据误差研究——以A股上市公司为例

|

胡国建(1992— ),男,江西九江人,讲师,主要研究方向为经济地理与区域发展。E-mail: guojianhu1992@163.com |

收稿日期: 2023-04-27

修回日期: 2023-06-24

网络出版日期: 2023-12-22

基金资助

国家自然科学基金项目(42171171)

国家自然科学基金项目(42361050)

Errors in statistical data from the perspective of corporate location: A case study of A-share listed companies

Received date: 2023-04-27

Revised date: 2023-06-24

Online published: 2023-12-22

Supported by

National Natural Science Foundation of China(42171171)

National Natural Science Foundation of China(42361050)

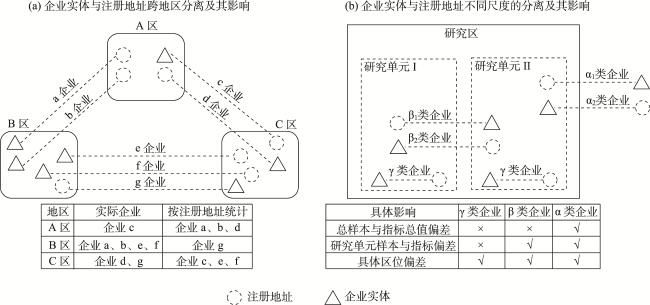

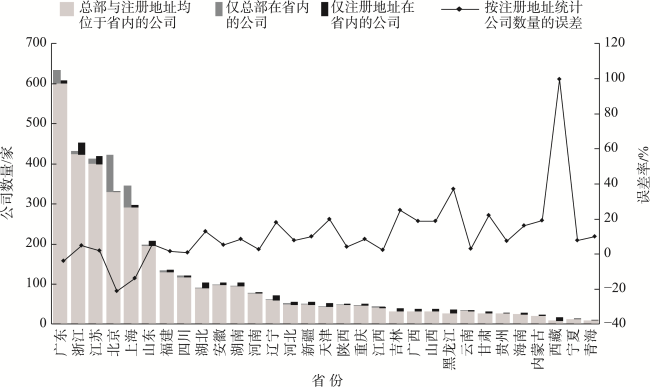

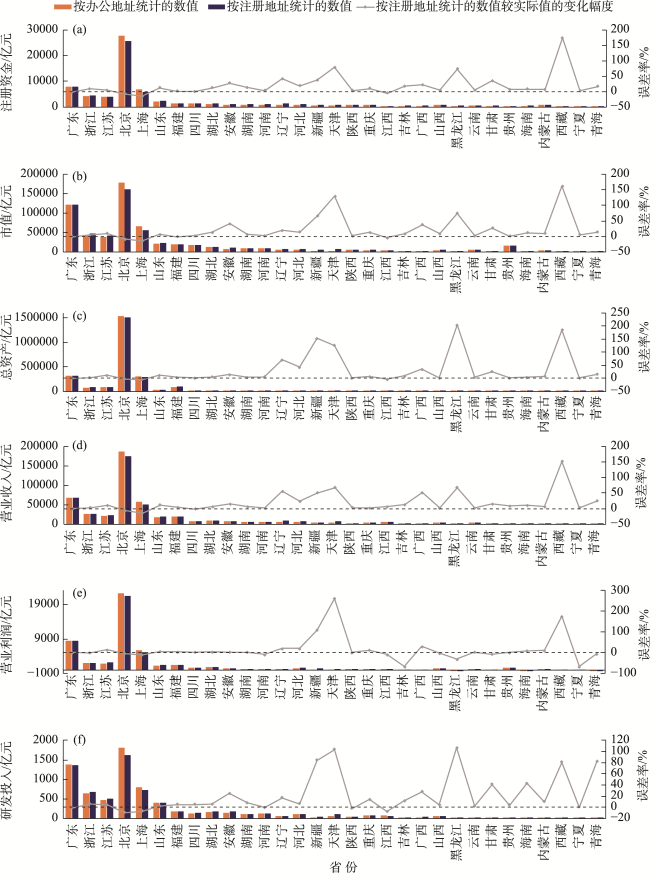

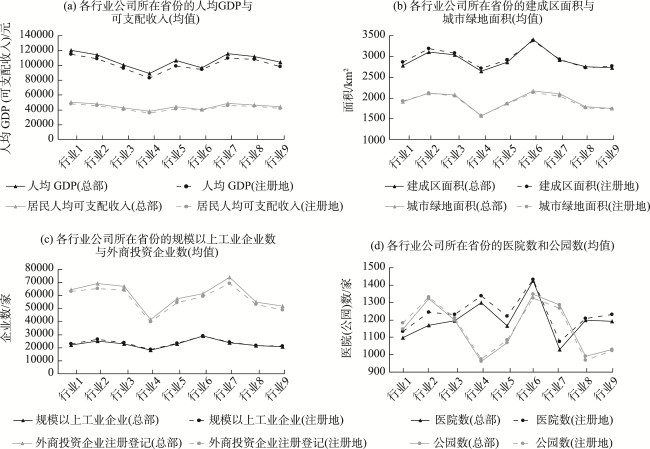

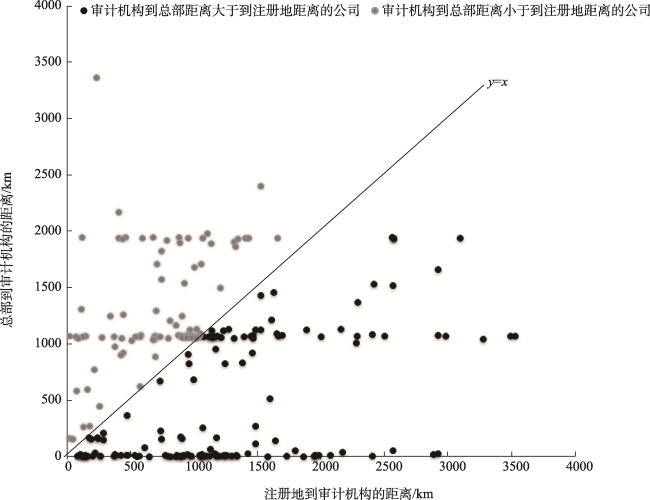

减少统计数据误差,提高数据质量对保障政府和企业的合理决策以及大量实证研究结论的可靠性具有重要意义。论文鉴于众多社会经济数据按企业注册地址进行统计,提出造成数据统计误差的新视角——企业实体位置与注册地址的空间分离,并以A股上市公司为例,考察公司数量、公司指标、发展环境指标(地区指标)以及地理距离等4类数据在省级尺度上按注册地址统计的误差幅度。研究显示,若按注册地址统计:各省上市公司数量的误差率平均为14.23%,6项公司指标归并的误差率平均为24.84%,且不同省份、不同指标的误差率差异较大;各行业上市公司按注册地址统计其8项地区指标平均误差率为3.04%,误差率较小;许多公司在总部所在地聘用会计师事务所,造成按注册地址计算上市公司到会计师事务所的地理距离会明显高于实际值。总体而言,企业实体与注册地址的分离现象对各类按后者统计的社会经济数据造成了不可忽视的误差影响,经济地理学对此应予以重视。

胡国建 , 陆玉麒 , 钟业喜 . 企业区位视角下的数据误差研究——以A股上市公司为例[J]. 地理科学进展, 2023 , 42(12) : 2309 -2323 . DOI: 10.18306/dlkxjz.2023.12.003

Statistical data errors not only mislead the analysis, decision making, and actions of the government, business, and individuals, but also cast doubt on the conclusions of numerous academic studies. Among these data, social-economic data related to businesses is an important target of statistical work, and the determination of business locations is a prerequisite for statistical data on businesses. Currently, the registered address serves as the business location in many social-economic data, but the phenomenon of spatial separation between confirmed business entities and registered addresses may result in significant errors when statistics are conducted based on registered addresses. This article argued that the spatial separation between business entity locations and registered addresses is a new perspective for understanding and studying statistical data errors, providing the possibility to measure actual data errors. In addition to the registered address, listed companies also disclose their office address, which serves as a breakthrough point for quantifying the separation between business entities and registered addresses and studying the statistical errors in data. Taking the office address as the geographical location of A-share listed company headquarters and using various types of data based on this location as the correct values, this study compared and analyzed the errors in data collected based on the registered address (including the number of companies, company indicators, regional indicators, and geographical distances). The study showed that when statistics are generated based on the registered address, the 233 A-share listed companies examined in this study are misclassified in terms of their province (that is, the headquarters are located in a province that is different from the registered address), with most of these companies being located in economically developed regions such as Beijing, Shanghai, and Guangdong, while the distribution of registered addresses is relatively scattered. Influenced by these companies, the average error rate of the number of companies calculated based on the registered address is 14.23% per province, indicating a more imbalanced distribution of the actual headquarter locations of listed companies compared to the registered addresses. The combined average error rate of the six company indicators is 24.84%, showing significant variation in error rates across different provinces and indicators. The average error rate of calculating eight regional development indicators based on the registered address for companies in different industries is 3.04%, indicating a relatively small error rate. The statistical error in calculating the geographical distance between companies and accounting firms based on the registered address depends on the location relationship between the headquarters, registered addresses, and accounting firms. Many companies hire accounting firms in their headquarter locations, leading to a significantly higher geographical distance calculated based on the registered address compared to the actual value. The issue of statistical data errors caused by the spatial separation between business entities and registered addresses will persist in the long term. Given the significant impact of data errors on government decision making, business strategy formulation, academic research, and so on, it is essential for the academic community, especially those in economic geography, to pay attention to the statistical data errors caused by the separation between business entities and registered addresses and their negative effects.

Key words: enterprise entity; registered address; headquarter; listed company; data error

表1 223家公司总部与注册地址的省份分布Tab.1 Distribution of the office addresses and registered addresses of 233 companies by province |

| 总部 所在 省份 | 注册地所在省份 | |||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 浙江 | 江苏 | 湖北 | 山东 | 辽宁 | 天津 | 黑龙江 | 西藏 | 湖南 | 广东 | 吉林 | 河北 | 新疆 | 广西 | 安徽 | 福建 | 上海 | 四川 | 甘肃 | 山西 | 重庆 | 海南 | 陕西 | 内蒙古 | 江西 | 河南 | 云南 | 北京 | 贵州 | 青海 | 宁夏 | 合计 | |

| 北京 | 8 | 5 | 5 | 6 | 4 | 9 | 7 | 1 | 2 | 6 | 4 | 6 | 4 | 1 | 1 | 4 | 2 | 1 | 2 | 2 | 2 | 4 | 3 | 1 | 1 | 1 | 92 | |||||

| 上海 | 15 | 11 | 1 | 2 | 3 | 1 | 2 | 2 | 2 | 2 | 2 | 2 | 4 | 2 | 2 | 1 | 54 | |||||||||||||||

| 广东 | 4 | 1 | 2 | 3 | 3 | 3 | 2 | 1 | 2 | 3 | 1 | 1 | 1 | 2 | 1 | 1 | 2 | 33 | ||||||||||||||

| 江苏 | 1 | 2 | 3 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 13 | |||||||||||||||||||||

| 浙江 | 1 | 1 | 1 | 2 | 1 | 2 | 1 | 9 | ||||||||||||||||||||||||

| 四川 | 2 | 1 | 1 | 1 | 5 | |||||||||||||||||||||||||||

| 福建 | 2 | 1 | 1 | 4 | ||||||||||||||||||||||||||||

| 江西 | 1 | 1 | 1 | 3 | ||||||||||||||||||||||||||||

| 河北 | 1 | 1 | 1 | 3 | ||||||||||||||||||||||||||||

| 陕西 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 天津 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 山东 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 湖北 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 新疆 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 重庆 | 1 | 1 | 2 | |||||||||||||||||||||||||||||

| 湖南 | 1 | 1 | ||||||||||||||||||||||||||||||

| 辽宁 | 1 | 1 | ||||||||||||||||||||||||||||||

| 安徽 | 1 | 1 | ||||||||||||||||||||||||||||||

| 河南 | 1 | 1 | ||||||||||||||||||||||||||||||

| 云南 | 1 | 1 | ||||||||||||||||||||||||||||||

| 合计 | 30 | 20 | 14 | 13 | 12 | 11 | 10 | 9 | 9 | 8 | 8 | 7 | 7 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 4 | 4 | 4 | 4 | 3 | 2 | 2 | 2 | 1 | 1 | 233 |

| [1] |

|

| [2] |

毛刘乐, 盛科荣, 张杰, 等. 金融网络嵌入对中国城市创业活力的影响研究[J]. 地理科学进展, 2022, 41(12): 2244-2257.

[

|

| [3] |

章屹祯, 汪涛, 张晗. 基于金融细分行业的长三角城市网络的组织模式及驱动因素[J]. 地理科学进展, 2022, 41(4): 567-581.

[

|

| [4] |

赵龙凯, 彭传国. 封闭式基金折价与管理绩效的实证研究[J]. 金融研究, 2008(4): 102-121.

[

|

| [5] |

钱肖颖, 孙斌栋. 基于城际创业投资联系的中国城市网络结构和组织模式[J]. 地理研究, 2021, 40(2): 419-430.

[

|

| [6] |

|

| [7] |

|

| [8] |

|

| [9] |

|

| [10] |

郭富青. 我国企业住所与经营场所分离与分制改革的法律探析[J]. 现代法学, 2020, 42(2): 145-156.

[

|

| [11] |

郭富青. 我国企业住所制度及改革的法理检讨与前瞻性构想[J]. 上海政法学院学报(法治论丛), 2020, 35(2): 87-104.

[

|

| [12] |

汪雨卉. 多源大数据视角下上海市初创企业集聚演化特征研究[D]. 上海: 上海师范大学, 2019.

[

|

| [13] |

|

| [14] |

陈林. 中国工业统计的理论体系与制度变迁: 兼议中国工业企业数据的部分系统性误差[J]. 经济科学, 2019(4): 69-80.

[

|

| [15] |

|

| [16] |

|

| [17] |

|

| [18] |

|

| [19] |

陈冬华, 胡晓莉, 梁上坤, 等. 宗教传统与公司治理[J]. 经济研究, 2013(9): 71-84.

[

|

| [20] |

刘磊. 我国A股市场地域联动性的实证研究[D]. 大连: 东北财经大学, 2016.

[

|

| [21] |

谭劲松, 陈艳艳, 谭燕. 地方上市公司数量、经济影响力与企业长期借款: 来自我国A股市场的经验数据[J]. 中国会计评论, 2010, 8(1): 31-52.

[

|

| [22] |

潘峰华, 夏亚博, 刘作丽. 区域视角下中国上市企业总部的迁址研究[J]. 地理学报, 2013, 68(4): 449-463.

[

|

| [23] |

胡国建, 金星星, 陆玉麒, 等. 中国上市公司总部与注册地跨城市分离的格局、形成过程和影响因素[J]. 地理研究, 2021, 40(2): 402-418.

[

|

| [24] |

沈甜甜, 汪洋. 上市公司地理位置、风险投资参与与股票流动性: 基于创业板市场的实证研究[J]. 金融理论与实践, 2020(8): 85-95.

[

|

| [25] |

曹洁. 金融集团内的信息流动与基金投资业绩[D]. 马鞍山: 安徽工业大学, 2012.

[

|

| [26] |

龙小宁, 林志帆. 中国制造业企业的研发创新: 基本事实、常见误区与合适计量方法讨论[J]. 中国经济问题, 2018(2): 114-135.

[

|

| [27] |

胡国建, 陆玉麒, 胡舒云. 顾及企业注册地址的区位理论研究[J]. 地理研究, 2022, 41(2): 580-595.

[

|

| [28] |

|

| [29] |

李汉青, 袁文, 马明清, 等. 珠三角制造业集聚特征及基于增量的演变分析[J]. 地理科学进展, 2018, 37(9): 1291-1302.

[

|

| [30] |

欧阳艳艳, 黄新飞, 钟林明. 企业对外直接投资对母国环境污染的影响: 本地效应与空间溢出[J]. 中国工业经济, 2020(2): 98-121.

[

|

| [31] |

|

| [32] |

王志高, 王如玉, 梁琦. 企业创新成功率与城市规模[J]. 统计研究, 2016, 33(7): 55-63.

[

|

| [33] |

|

| [34] |

郭军. 审计师的地理邻近性与客户公司的股价崩盘风险[D]. 厦门: 厦门大学, 2018.

[

|

| [35] |

周嘉妮. 分所层面客户重要性、地理因素对内部控制审计质量的影响研究[D]. 厦门: 厦门大学, 2019.

[

|

| [36] |

罗进辉, 李雪, 林芷如. 审计师—客户公司的地理邻近性与会计稳健性[J]. 管理科学, 2016, 29(6): 145-160.

[

|

| [37] |

朱敏, 汪传江. 企业空间区位会影响分析师IPO定价预测的准确性吗?[J]. 财经论丛, 2017(10): 60-70.

[

|

| [38] |

陈青雁, 王鹏, 钟业喜. 中国民营上市企业总部空间格局及影响因素[J]. 世界地理研究, 2020, 29(5): 996-1005.

[

|

| [39] |

蒋子龙, 王军, 樊杰. 1990—2019年中国上市公司总部分布变迁及影响因素[J]. 经济地理, 2022, 42(4): 112-121.

[

|

| [40] |

王晶. 我国宏观经济统计数据质量诊断方法与实证[J]. 统计与决策, 2018, 34(4): 34-37.

[

|

| [41] |

|

| [42] |

文嫮, 张强国, 杜恒, 等. 北京电影产业空间集聚与网络权力分布特征研究[J]. 地理科学进展, 2019, 38(11): 1747-1758.

[

|

| [43] |

汲昌霖. 政治关联是否促进了企业绩效: 基于金融生态环境的视角[J]. 公司金融研究, 2015(3): 45-58.

[

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}