An overview of offshore financial centers from a geographical perspective

PAN Fenghua1, 2, , ZENG Beini1, 2

1. School of Geography, Faculty of Geographical Science, Beijing Normal University, Beijing 100875, China2. Beijing Key Laboratory of Environmental Remote Sensing and Digital City, Faculty of Geographical Science, Beijing Normal University, Beijing 100875, China

After the Second World War, financial globalization, an important component of economic internationalization, has become a key characteristic of the global economic development. Offshore financial centers are developed under the background of financial internationalization and innovation, and play an important role in promoting development and change of capital organization and emerging markets. Because of their unique geographical distribution and important role in the global economy and financial system, geographers have begun to study offshore financial centers. In this article, we reviewed the literature on offshore financial centers in geography. We first introduced the related concepts and changes, then examined the following topics: the location and development conditions of offshore financial centers, their regional and global influences, the interaction between offshore financial centers and the global financial system, and their development in China. Moreover, we discussed how to research offshore financial centers from a geographical perspective in the future.

Keywords:offshore financial center

;

global financial network

;

tax heaven

;

locational conditions

;

geography

PANFenghua, ZENGBeini. An overview of offshore financial centers from a geographical perspective[J]. Progress in Geography, 2019, 38(2): 191-204 https://doi.org/10.18306/dlkxjz.2019.02.004

离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位。2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010)。不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015)。据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所。金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010)。

由于离岸金融中心在全球经济金融体系中的重要地位及其显著的区位特征,受到了地理学研究的广泛关注。离岸金融中心本身就有一个独特的地理视角,这些公司和个人作为发起方,因为税收、监管和保密等原因,注册和投资到母国之外的地方,加剧了资本在空间上的流动和集聚。分散来看,离岸金融中心只是一个个资本周转地,但综合所有的离岸金融中心可以让我们更好地了解现代金融体系网络化的运作模式(Lewis et al, 1987)。

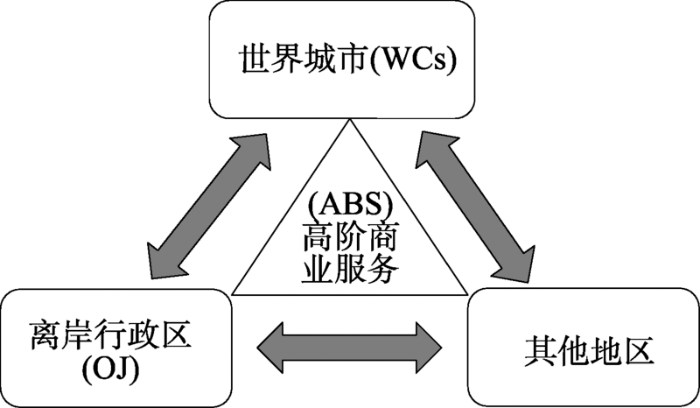

地理学者从20世纪90年代开始关注这方面的问题。较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化。随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位。但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997)。近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015)。在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角。全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ)。离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系。

离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994)。随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚。这种观点强调离岸金融中心是虚拟的、随机的。第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的。这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的。Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性。Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生。还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014)。Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动。他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展。孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础。由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心。

从另一方面来说,当地政府或货币当局对其货币金融的管制加强或放松也是影响离岸金融中心产生的因素。第一种形式是对在岸政府监管加强的回应,Johns(1983)将政府干预市场的行为用“摩擦力”的概念来描述,离岸金融中心的环境比在岸市场更为宽松,因此存在很小甚至为零的“摩擦力”,也就推动了离岸金融中心的经营和发展。第二种形式是通过政策直接推动当地离岸金融中心的发展,这种离岸金融中心以发展离岸国际金融业务为主要特色,如开曼群岛、巴哈马、泽西岛等。另外,因为缺乏一些监管机构,“逃税”可能成“合理”的行为,一些法律还不是很健全的发展中国家更容易出现离岸金融中心,而且发展迅速(Clark et al, 2015)。除此之外,国际政治经济环境、地理位置便利、政局稳定、自然灾害少、基础设施完善、金融法律服务专业、金融法律健全、政策优惠也是离岸金融中心形成的主要区位条件(杨叠涵等, 2013; 孟广文等, 2017)。

Fig.2 Interactive relationship between offshore financial centers (OFC) and the global financial system

3.1 离岸金融中心与高阶商业服务(ABS)公司的 关系

离岸金融活动的实质就是资金在离岸金融中心与其他空间之间的流动,这些流动依靠跨国公司、富人和政府的对外投资来完成,而高阶商业服务(ABS)公司在这些个体产生相互作用的过程中起到了中介的作用。由于ABS公司拥有丰富的信息来源和专业技能,无论是跨国公司还是政府,都需要ABS公司的协助。跨国公司利用ABS公司来帮助他们筹集资金,了解外国法律法规和市场,而政府需要ABS公司来帮助他们制定合适的政策吸引跨国公司来此投资(Büthe et al, 2011)。从人员构成来说,ABS公司也是金融精英、税务精英的集聚地,这些精英运用自身的专业知识和社会网络帮助企业和富人运转资金,并精心设计流程使得纳税义务最小化。Eden等(2005)提出,要理解离岸金融中心与在岸空间的互动关系,来自离岸金融中心的税务精英是一个很重要的切入点。Wainwright(2011)在英国住房抵押贷款证券化的研究中也发现,离岸金融的活动是一些金融专业人士群体和他们的客户通过紧密联系的社会网络架构而成,税务精英在投资网络中处于中心地位。他探究在信贷危机发生时,税务精英们如何利用立法漏洞使得“税务最小化”的策略得以实现,推动了英国经济金融化,但同时增加了信贷危机暴露的严重程度。Buckley等(2015) 以中国跨国公司为例,发现跨国公司是基于金融关系的网络,这些金融精英们的行为会影响资金的流动,从而对离岸金融中心和在岸空间的相互作用产生影响。

离岸金融中心经常拿来与国际金融中心(International Financial Center, IFC)作比较,两者都处于全球金融体系的中心地位,是世界上最富裕的地方,因为它们运作着全球大部分的资金。一方面,这种相似性可能导致两者的竞争,国际金融中心虽然拥有健全的法律体系,却不能用低税率和保密法吸引到更多的企业和富人,于是一些国际金融中心也开始办理离岸业务,在岸(Onshore)和离岸的界限也越来越模糊,甚至还出现了一种所谓“中间岸”(Mid-shore)的行政区,例如中国香港和新加坡,它们综合了离岸的优势(低税率,保密)和一些在岸的特征(健全的法律体系、双边贸易协定、复杂的金融市场),一些在岸行政区甚至比离岸行政区拥有更加宽松的政策(Clark et al, 2015)。如今,离岸中的“岸”已演化成为虚拟的岸,离岸金融的意义逐渐演变为制度性而非地域性。

地理学者大约从20世纪90年代开始关注离岸金融中心,经过近30 a的研究,对离岸金融中心的认识逐步深化。早期的研究主要关注离岸金融中心的避税功能,后来开始关注保密等其他方面的功能(Hampton et al, 1999; Cobham et al, 2015),逐渐形成一个综合全面的视角。地理学的研究特色在于其独特的空间和网络视角:从微观尺度来说,每个离岸金融中心的地理位置、经济水平、殖民关系都不相同,这些地方特性能决定它们向不同方向发展;从宏观尺度来说,离岸金融中心只是全球金融体系中的一个组成部分,它们与其他组成部分之间会通过资金流动或社会关系而产生相互作用,把这些联系综合起来,也就形成了全球离岸金融的网络。

在研究内容上,地理学早期的文献回答了许多关于离岸金融的基本问题,如离岸金融的概念、功能分类,离岸金融中心形成和发展的影响因素,离岸金融中心对全球和区域的影响等,这些研究比较成熟,且分析以案例为主,关注单个离岸金融中心的发展历程。近年来,地理学者视野更加开阔,开始关注离岸金融中心与全球金融体系中其他成分的相互作用关系,尝试解释离岸金融中心与全球金融体系的互动关系;还有学者着眼于全球,探索离岸金融中心的地理分布特征,展现不同类型和尺度的离岸金融网络。由于离岸金融中心是一个高度综合的话题,地理学家结合经济学、金融学、政治学、社会学的研究方法,开始尝试使用不同的概念框架理解离岸金融中心在世界经济体系中的地位,例如全球金融网络(GFN)、全球价值链(Global Value Chain, GVC)、国际商业(International Business, IB)等,从不同尺度重新认识全球离岸金融格局,但这部分研究相对来说还比较不成熟,还有较大的发展空间。

事实证明,流向离岸金融中心的资金不一定总是流向监管最宽松的司法行政区,而是流向那些监管制度最有利于具体操作的司法行政区(Aalbers, 2017),而这个“利”往往涉及政治利益、经济利益和社会声誉等等,因此,今后的地理学对离岸金融中心的研究不仅要关注经济层面,更要与政治、社会学有交叉,这样才能帮助我们更好地理解离岸金融中心的起源、发展和未来趋势。除此之外,在全球化与金融化导致全球经济发展越来越不均衡的背景下,离岸金融业务和市场的内涵日趋复杂,离岸金融中心的空间格局可能会有所改变。由于传统离岸金融中心的衰落和新兴金融中心的崛起而重塑的新离岸金融格局以及背后的影响因素和作用机制都值得地理学再去探寻,同时也需要学者找寻新的视角来看待这些问题。对中国来说,在外商投资方面,自改革开放以来,以英属维尔京群岛、开曼群岛等为代表的避税港型离岸金融市场的对华投资额就一直保持前列(孟广文等, 2017),而大部分中国在海外上市的企业也选择这些离岸金融中心作为注册地(Pan et al, 2014),这种现象背后的原因以及中国如何融入全球离岸金融网络也值得地理学者思考。

The authors have declared that no competing interests exist.

Received internationalization theory argues that firms occupy domestic space before going abroad; in other words, large, oligopolistic firms are most likely to internationalize. The experience of China, whose economy is fragmented and whose firms are small by global standards, suggests otherwise. We construct a model of small firm internationalization driven by the relative transaction costs of crossing domestic (in the case of China, provincial) and international borders. When the costs of crossing domestic borders exceed the costs of crossing international borders, firms will internationalize at a relatively early stage of development. In the case of China, local protectionism and inefficient domestic logistics increase the costs of doing business domestically; moreover, protection of property rights in the West and the advantages afforded Chinese owned firms reconstituted as foreign entities operating in China decrease the costs of 'going out'. We coin the term 'institutional arbitrage' to capture Chinese firms' pursuit of efficient institutions outside of China. We argue that strategic exit from the home country rather than strategic entry into foreign markets may explain the internationalization of many Chinese firms.

[19]

BooijinkL, WeyzigF.2007.

Identifying tax havens and offshore finance centres

[R/OL]. Tax Justice Network Working Paper. [2018-08-16]..

A large share of the outward foreign direct investment (FDI) of emerging market MNEs is directed towards a small number of specific tax havens and offshore financial centres. The establishment of investment-holding companies for taxation related purposes is frequently adduced as a key motivation (0900round-tripping0964) for these investments. This explanation, however, accounts for neither the concentration of such investments in specific havens nor the comparatively large national shares of such investments that originate from emerging markets. Here we draw from and build links between the geography of money and finance and international business literatures to conceptually and empirically explore this prominent, if somewhat disregarded, feature of global FDI flows.

[22]

BütheT, MattliW.2011. The new global rulers: The privatization of regulation in the world economy [M]. Princeton: Princeton University Press.

Recent scandals involving large corporations including Amazon, Apple, Google, Starbucks, and HSBC have highlighted the problems of tax avoidance, evasion, and offshore financial activities. Considering their significance to growing inequality and financial instability, renewed media and public attention is well justified, and new research on these topics urgent. At the same time, however, there is confusion in the very use of the term offshore finance. Some apply it interchangeably with tax havens; others go as far as to use it as a synonym of international finance. We argue that offshore finance needs a precise definition and careful positioning in a broader economic geographical framework. We suggest a definition based on the legal and accounting, in addition to financial, aspects of offshore finance, and we propose the concept of global financial networks to situate offshore jurisdictions and offshore finance in the firm erritory nexus and in relation to global production networks. This sets the stage for the three research articles presented in this issue, which map offshore financial networks at global and regional scales, and investigate their causes and mechanisms.

[27]

Cobb SC.1998.

Global finance and the growth of offshore financial centers: The Manx experience

The globalization of the world economy and the concomitant increasing complexity of the global financial system has resulted in a large number of relatively small places functioning as offshore financial centers (OFCs). OFCs provide an alternative avenue for capital to be invested (literally) in offshore markets. This paper argues that these small places have to strive hard to link in to the global economy in a reputable fashion and have to do so through the creation of spatially focused financial regulation and supervision. The importance of the constructs of trust, knowledge, reputation, and networks in the functioning of offshore financial services is explored. A conceptual framework is developed to illustrate how OFCs link in to the global economy along three dimensions: regulation, location, and function. A case study of the rise of the Isle of Man as an OFC provides empirical evidence regarding global-local linkages and the importance of creating an appropriately balanced regulatory regime.

[28]

CobhamA, JanskýP, MeinzerM.2015.

The financial secrecy index: Shedding new light on the geography of secrecy

Both academic research and public policy debate aroundtax havensandoffshorefinance typically suffer from a lack of definitional consistency. Unsurprisingly then, there is little agreement about which jurisdictions ought to be considered as tax havens r which policy measures would result in their not being so considered. In this article we explore and make operational an alternative concept, that of asecrecy jurisdictionand present the findings of the resulting Financial Secrecy Index (FSI). The FSI ranks countries and jurisdictions according to their contribution to opacity in global financial flows, revealing a quite different geography of financial secrecy from the image of small island tax havens that may still dominate popular perceptions and some of the literature onoffshore finance. Some major (secrecy-supplying) economies now come into focus. Instead of a binary division between tax havens and others, the results show a secrecy spectrum, on which all jurisdictions can be situated, and that adjustment for the scale of business is necessary in order to compare impact propensity. This approach has the potential to support more precise and granular research findings and policy recommendations.

[29]

Coe NM, Lai K PY, WójcikD.2014.

Integrating finance into global production networks

Coe N. M., Lai K. P. Y. and Wójcik D. Integrating finance into global production networks, Regional Studies. While successful in its aim of ‘globalizing’ regional development, the global production network (GPN) approach has thus far paid less attention to the role of finance in the dynamics of the global economy and regional development. This lacuna is significant as finance is arguably even more globalized and networked than production. To address this gap the paper distils the concept of the global financial network (GFN) from financial geography and related scholarship, with advanced business services, world cities and offshore jurisdictions at the core. Interactions between the GPN and the GFN are discussed, focusing on the financing and financializing of GPNs and the co-evolution of globalization and financialization. Integrating finance into GPN research entails more than a simple extension of the approach; it would also enrich it conceptually, and enable it methodologically and empirically.

[30]

Coe NM, Yeung HW.2001.

Geographical perspectives on mapping globalisation: An introduction to the JEG special issue mapping globalisation: Geographical perspectives on international trade and investment

[J]. Journal of Economic Geography, 1(4): 367-380.

Taxing multinational enterprises (MNEs) is inherently conflictual because national tax systems are not well designed to handle their international activities. The OECD has been instrumental in developing an international tax regime to govern the conflicts and interdependencies induced by national taxation of MNEs. The strength of this regime depends on the extent to which states adhere to the regime's norms and practices. We examine the OECD's Harmful Tax Competition initiative, arguing that tax havens have been as renegade states in the international tax regime. We explore how the OECD initiative developed and evaluate its impact on regime effectiveness.

[35]

FernandezR, WiggerA.2016.

Lehman Brothers in the Dutch offshore financial centre: The role of shadow banking in increasing leverage and facilitating debt

(2016). Lehman Brothers in the Dutch offshore financial centre: the role of shadow banking in increasing leverage and facilitating debt. Economy and Society: Vol. 45, No. 3-4, pp. 407-430. doi: 10.1080/03085147.2016.1264167

While most research on FDI focuses on the ‘real’ economy, at least 30% of global FDI stock is intermediated through tax havens. Using 2010 IMF data on FDI stock

[39]

HaberlyD, WójcikD.2015.

Regional blocks and imperial legacies: Mapping the global offshore FDI network

While FDI is generally assumed to represent long-term investments within the “real” economy, approximately 30-50% of global FDI is accounted for by networks of

[40]

HallS.2017.

Rethinking international financial centres through the politics of territory: Renminbi internationalisation in London's financial district

[J]. Transactions of the Institute of British Geographers, 12(9): 4437

The Jersey island Offshore Finance Centre (OFC) model may be used for other Small Island Economies (SIEs) wishing to exploit offshore finance as a development option. Although the Jersey model can not be copied precisely by other SIEs, the key factors of political stability, minimal regulation, secrecy, low tax, proximity to a large developed economy and basic communication links could allow certain islands to host OFCs. The benefits of hosting an OFC outweigh the costs, and the increasing global offshore market indicates potential income generation for some OFCs located near the emerging supra-regional blocs.

[42]

Hampton MP.1996.

Where currents meet: The offshore interface between corruption, offshore finance centres and economic development

SummaryThe connections between economic development, corruption and the increasingly globalized financial system are not yet fully understood. In this article we examine tax havens and Offshore Finance Centres (OFCs) which form an interface between developed countries and LDCs. The central argument is that the existence of these financial channels facilitates and can even encourage onshore corruption. The combination of new technology with strict bank secrecy in the 'private banking' offshore networks of major banks allows rapid and non-transparent international flows of funds, creating an increasing synergy between the offshore interface, globalization and onshore corruption.

[43]

Hampton MP, Christensen JE.1999.

Treasure Island revisited. Jersey's offshore finance centre crisis: Implications for other small island economies

[J]. Environment and Planning A, 31(9): 1619-1637.

A dominant story about globalization tells of relatively immobile places, seeking to attract increasingly mobile capital, becoming locked into a process of competitive deregulation. This paper argues that such a story is based on an increasingly inaccurate and unhelpful conceptualization of place. Massey's idea of place as socially constructed nexus is presented as a better starting point for examining the position of places within a globalizing economy. The social construction of the Bahamas and Cayman as places for offshore finance is investigated, paying particular attention to the positions and roles of multinational banks and governments. Even within the sphere of offshore finance in which capital is highly mobile, the dominant story of place competition and competitive deregulation is far from convincing. Globalization does not inevitably lead to place competition because in changing the positions, powers and scales of operation of the state and non-state actors which make places what they are, globalization actually alters the nature of places. Although places are socially constructed and hence dynamic, the meanings of places are temporarily stabilized through processes of scaling and the drawing of borders. For places to be stabilized there must be trust among the various actors involved in their social construction. The necessity of trust rules out processes of competitive deregulation which might erode the very social foundation of places. This is particularly so during an era of globalization in which places are remade and their borders redrawn by a wide variety of local and extra-local actors.

[45]

Hudson AC.1999.

Off-shores on-shore: New regulatory spaces and real historical places in the landscape of global money

[M]// MartinR. Money and the space economy. London, UK:Wiley: 139-154.

Processes of globalization rework sovereignty as the ordering principle of the international political economy, creating new geographies of power. Such a reworking is most apparent offshore, a site where sovereignty is unbundled. The principle of sovereignty is maintained in the offshore financial centres' legal sovereignty but relinquished in terms of their fiscal powers. This unbundling articulates the state system and the capitalist economy. Such an unbundling is possible because sovereignty is based upon property rights. Changes in the practices and understandings of property rights change the meaning of sovereignty, altering the principle of differentiation which shapes the international political economy. In this way, the paradoxical marginality and centrality of offshoreness to the dynamics of the international political economy is explained.

[47]

Johns RA.1983. Tax havens and offshore finance: A study of transnational economic development [M]. London, UK: Bloomsbury Publishing.

This study examines the changing competitiveness of financial centres in mainland China and Hong Kong based on the geography of equity listing of mainland Chinese firms. Pre-listing firm characteristics are used to explore firms' motives for listing on a particular exchange and whether these motives have changed over time. The results show that Hong Kong's prominence as an international financial centre is attracting the largest and, recently, also the best performing mainland Chinese state-owned enterprises to go public. Less differentiation exists between the competitiveness of Shanghai and Shenzhen, although the renewed strategy of the Shenzhen stock exchange to attract smaller firms appears to be successful. [PUBLICATION ABSTRACT]

[49]

LaiK.2011.

Marketization through contestation: Reconfiguring China's financial markets through knowledge networks

[J]. Journal of Economic Geography, 11(1): 87-117.

Abstract This article unpacks a particular case of market making by scrutinizing the richness of market meanings, the diversity of market actors and the contested nature of market knowledge and practices, in the context of developing banking regulation and financial services in China. Based on personal interviews and secondary data, it examines how China's financial markets are reconfigured through heterogeneous knowledge networks ranging from mobile transmigrants and regulatory counterparts in other countries to different financial institutions within China. China's WTO accession is not a straightforward liberalization of its banking sector but a contested process of negotiations between the Chinese government, regulatory bodies and foreign and domestic banks. This process of knowledge translation and conflict resolution is key to revealing the temporary and unstable character of markets and demonstrates how the entanglement of different knowledge networks opens up conjectural space for new forms of market meanings and practices. The Author (2010). Published by Oxford University Press. All rights reserved.

[50]

LaiK.2012.

Differentiated markets: Shanghai, Beijing and Hong Kong in China's financial centre network

We document and assess the role of small financial centres in the international financial system using a newly assembled data set. We present estimates of the foreign asset and liability positions for a number of the most important small financial centres and place these into context by calculating the importance of these locations in the global aggregate of cross-border investment positions. We also report data on bilateral cross-border investment patterns, highlighting which countries engage in financial trade with small financial centres.

[52]

LedyaevaS, KarhunenP, KosonenR, et al.2015.

Offshore foreign direct investment, capital round-tripping, and corruption: Empirical analysis of Russian regions

Recent economic geography research has identified the round-tripping of capital from emerging economies to offshore financial centers (OFCs) and back as foreign direct investment (FDI) as a central element of the global offshore FDI network. However, the factors behind this phenomenon are not yet fully understood. Our study develops a general framework that conceptualizes the phenomenon of round-trip investment. In particular, we argue that secrecy arbitrage, defined as interplay of onshore corruption and offshore secrecy, largely explains round-trip investment between onshore jurisdictions and OFCs. First, we argue that part of the round-trip FDI consists of proceeds from corruption, which is laundered in OFCs and reinvested back to the location of origin. Second, we maintain that the secrecy dimension of the OFC also motivates the round-tripping of licit capital, as businesses use the secrecy provided by OFCs to hide their true identities from corrupt authorities in the home location. To test the validity of our argument about onshore corruption as a driver for round-trip investment, we empirically analyze firm-level data on the distribution of offshore FDI (which, we argue, is largely round-trip) across Russian regions. Our empirical findings confirm that FDI from OFCs is positively associated with host region corruption, and this relationship is stronger for OFCs with a higher secrecy score. Hence, we conclude that round-trip FDI is strongly motivated by the interplay between onshore corruption and offshore secrecy.

[53]

Levich RM.1998.

Emerging market capital flows: Proceedings of a conference held at the Stern School of Business, New York University on May 23-24, 1996

In an economy characterized by financial repression, enhancing the legal system may hinder the development of some aspects of the financial sector, especially informal arrangements aiming at circumventing the repression. Using Chinese provincial data in the 1990s, we find that enhanced legal system suppresses private investment and has no effect on financial depth although it increases the private share of bank credits and bank competition. We interpret these findings as evidence showing the existence of the leakage effect that moves financial resources from the privileged state sector to the rationed private sector. In addition, we find that enhanced legal system does not have a significant effect on the average GDP growth rate. We conclude that the smooth functioning of the legal system requires other institutions to complement.

[59]

MartinR.1997.

The geography of finance: Spatial dimensions of intermediary behavior

[J]. Tijdschrift voor Economische en Sociale Geografie, 88(5): 501-502.

In a globalising world, as economies are becoming increasingly integrated the number of firms seeking to connect to global capital markets and list on international stock exchanges is rapidly rising. Up to 2011 there have been more than 1000 Chinese firms listed on overseas stock exchanges. As a dynamic and emerging economy, the connection of Chinese firms to global capital markets and flows has the potential to reshape economic geography at a variety of geographical scales. Despite this, there has been limited academic enquiry attending to these issues and exploring the internationalisation of Chinese firms through overseas listing. Using a comprehensive dataset, this paper addresses this research lacuna and provides a preliminary analysis of the geography of overseas listings. The paper describes how the trend and geography of Chinese firms listing overseas started in the late 1980s but has grown rapidly in the past decade. Hong Kong, New York, Singapore, and London are the major destinations of larger Chinese firms for overseas listing, while emerging destinations such as Germany, South Korea, Australia, and Canada are attracting more firms. We found that firms in different locations and sectors favoured different markets. Generally listing firms tend to originate from eastern China, reflecting the spatial pattern of the Chinese economy. The paper argues that there are two main factors influencing the geography of Chinese firms overseas listing activity. The first is the role of the state in influencing, and in some cases, directly determining the locational choice of overseas listing for Chinese firms. The second is the effect of proximity preferences in influencing the decision taken by some firms to list in particular overseas markets. The paper closes with a discussion on the impacts of overseas listings domestically in China and globally on international exchanges where firms list.

[68]

Park YS.1982.

The economics of offshore financial centers

[J]. Columbia Journal of World Business, 17(4): 31-35.

This article presents a history of international tax governance and offers a rationalist reconstruction of its trajectory. As an unintended consequence of its institutional setup, the tax regime, which originally only dealt with double tax avoidance, produces harmful tax competition. Despite this negative effect there are only incremental and partial changes of the regime, which are insufficient to curb tax competition. I argue that this development can be explained by considering the properties and the sequence in which they come up of the collective action problems inherent in double tax avoidance and tax competition. First, in double tax avoidance, a coordination game with a distributive conflict, governments did not want to endanger the solution they had institutionalized long before tax competition became virulent. Second, governments are unable to resolve the emergent asymmetric prisoner's dilemma of tax competition due to conflicts of interest among big and small country governments and successful lobbying of corporate capital. As a result, the institutional trajectory is characterized by the simultaneous occurrence of stability in the core principles and indirect and incremental changes of the rules in the form of rule stretching and layering.

[72]

RixenT.2013.

Why reregulation after the crisis is feeble: Shadow banking, offshore financial centers, and jurisdictional competition

A crucial element in the complex chain of factors that caused the recent financial crisis was the lack of regulation and oversight in the shadow banking sector, which is largely incorporated in offshore financial centers (OFCs), but instead of swift and radical regulatory reform in that sector after the crisis, we observe only incremental and ineffective measures. Why? This paper develops an explanation based on a two-level game. On the international level, governments are engaged in competition for financial activity. On the domestic level, governments are prone to capture by financial interest groups, but also susceptible to demands for stricter regulation by the electorate. Governments try to square the circle between the conflicting demands by adopting incremental and symbolic, but largely ineffective, reforms. The explanation is put to empirical scrutiny by tracing the regulatory initiatives on shadow banks and OFCs at the international level and within the United States and the European Union, where I focus on France, Germany, and the United Kingdom.

[73]

Roberts SM.1994.

Fictitious capital, fictitious spaces: The geography of offshore financial flows

[M]// Corbridge S, Martin R, Thrift N. Money, power, and space. Oxford: Blackwell: 91-115.

This paper examines the offshore financial center (OFC) of the Cayman Islands in the Caribbean as part of an attempt, on the one hand, to map emerging geographies associated with rapid and far-reaching changes in the international financial system, and, on the other hand, to further a Marxian understanding of how capital increases its flexibility and averts crisis (not unproblematically) through the financial system. Thus, in this paper, the major industries of the offshore sector in the Caymans are outlined and their development presented. I then examine the Cayman Islands'' development and operation as an OFC in two wider contexts: first, changes in the practice of international banking, and second, the regional competition between 090008entrepreneurial islands090009 for offshore finance. I argue that the development of new spaces in the global economy090000OFCs090000cannot be understood without an understanding of changes in the international financial system (new markets, instruments, risks, and others). Furthermore, the changes in the international financial system cannot be understood except as operating through space and specifically through distinct spaces such as the OFCs. Although the Cayman Islands are a small place, they have strategically positioned themselves at the nexus of the circuits of fast and fungible financial capital and offer a window on the workings of the international financial system.

[75]

Rose AK, Spiegel MM.2007.

Offshore financial centres: Parasites or symbionts?

This article analyses the causes and consequences of offshore financial centres (OFCs). While OFCs are likely to encourage bad behaviour in source countries, they may also have unintended positive consequences, such as providing competition for the domestic banking sector. We derive and simulate a model of a home country monopoly bank facing a representative competitive OFC which offers tax advantages attained by moving assets offshore at a cost that is increasing in distance to the OFC. Our model predicts that proximity to an OFC is likely to be pro-competitive. We test and confirm the predictions empirically. OFC proximity is associated with a more competitive domestic banking system and greater overall financial depth.

[76]

SassenS.2001. The global city: New York, London, Tokyo [M]. Princeton: Princeton University Press.

Purpose – This paper aims to explore the contribution of China's largest business groups to China's outward foreign direct investment (OFDI), looking particularly at the question of whether they contribute to strategic-asset-seeking OFDI. Design/methodology/approach – It uses national-level data and business group OFDI data to explore the sectors from which OFDI originates and destinations to which it is sent. From this conclusions are drawn as to the types of investments being made. Findings – In the national context strategic-asset-seeking OFDI from China has been rather limited to date. Instead, OFDI expansion still appears more closely linked to China's expansion as a trading nation with a natural resource deficit. Strategic-asset-seeking OFDI when it does take place, moreover, is orchestrated to a large extent through large state controlled business groups, as is much other OFDI. Research limitations/implications – A limitation of this research is the reliance on official data and the assumed simplification that most strategic-asset-seeking OFDI is concentrated in the manufacturing industries. Practical implications – More attention should be paid to the role of these select business groups as they play a significant part in China's OFDI. Originality/value – There is a growing presumption that much of China's OFDI is strategic-asset-seeking in nature and that new theories are required to explain this trend. Many firm-level studies, however, rely upon just a few high-profile but unrepresentative cases. This paper redresses this imbalance. It also shows that China's largest trial business groups have played an important role in her OFDI to date.

[83]

The Economist. 2013. Special report: Offshore finance

In what ways can we write about the ‘politics’ of international money? This paper is an attempt to answer this question in three different but related ways, each of which forms a major section of the paper. First, we attempt to describe international money as a hybrid of time, space and risk with increasingly formidable communicative demands. Second, we attempt to describe the structures of governance of international money, concentrating especially on the four main actor-networks of nation-states, the media, money capitalists and machines. Third, we try to settle some of the claims made in the previous two sections by reference to the de-traditionalization of the City of London over the last 30 years or so. The paper concludes with a short disquisition on the concept of the ‘public sphere’ as it might be applied to the world of international money.

[85]

Töpfer LM, HallS.2017.

London's rise as an offshore RMB financial centre: State-finance relations and selective institutional adaptation

China’s currency, the renminbi (RMB), is increasingly important in global financial markets, facilitated by the global expansion of offshore RMB centres. This paper examines London’s development as the first Western offshore RMB centre established in 2013, drawing on original research conducted between 2013 and 2015 in London and China. The longitudinal analysis reveals that the development of RMB finance in London is characterized by selective adaptation in which state–private bargaining dynamics have shifted from strategic alignment to a bifurcation of interests. Understanding these state–finance relations has important implications for research and policy-making concerned with (offshore) financial centres and RMB internationalization.

[86]

VlcekW.2011.

Byways and highways of direct investment: China and the offshore world

[J]. Journal of Current Chinese Affairs, 39(4): 111-142.

With the steady integration of a deregulated world of hypermobile capital, offshore banking has become an increasingly significant part of the geography of international finance. Many interpretations tend to treat offshore banking centres as identical sites of investment that can be easily substituted for one another by completely mobile, fungible capital. This paper explores the nature of offshore banking in one largely overlooked centre, Panama. It charts the historic context that led to the creation of Latin America's most important centre of international banking, emphasizing the unique qualities that stand in contrast to hyperglobalist interpretations, including the Canal and the role of the US dollar. Second, it summarizes the regulatory changes initiated in the face of global neoliberalism, including the absence of a central bank and recent reforms designed to attract foreign capital. Using primary and secondary data, the paper maps Panama's growing role as a net capital exporter, charting domestic and foreign loan markets. Finally, it also addresses the trade090009offs between confidentiality, and transparency in the context of illicit activities frequently alleged to occur in offshore banking centres, which in Panama revolve around drug trafficking and money laundering. It concludes by noting that even in an ostensibly seamless world, offshore banking exhibits the place090009based embeddedness of financial capital within local institutional relations.

[90]

WójcikD.2013

a. The dark side of NY-LON: Financial centres and the global financial crisis

This paper brings financial centres into the debate on the causes and consequences of the global financial crisis, by focusing on New York and London. It argues that the degree of commonality, complementarity and connectivity between the two leading global financial centres justifies the use of the term the New York-London axis' (the axis). It shows that the global financial crisis 2007-09 originated to large extent in the axis rather than in an abstract space of financial markets. The dominance of the axis in global finance can be easily underestimated and evidence suggests that, contrary to expectations the axis is not in decline. The main implication is that the debate on global financial reform has to take seriously the reality of global financial centres. In particular, if global finance is to change, the New York-London axis has to change.

[91]

WójcikD.2013b.

Where governance fails: Advanced business services and the offshore world

The paper analyses the evolution of China Mobile – one of China's pioneer ‘national champions’, and one of the world's largest telecom companies – through the lens of global financial networks, focusing on the role of advanced business services, financial centres and offshore jurisdictions in economic development. It demonstrates that despite being a domestic company, China Mobile is plugged firmly into the global financial networks, with incorporation in Hong Kong, cross-listing in Hong Kong and New York, and opaque offshore companies registered in the British Virgin Islands. Global advanced business services firms, with Goldman Sachs in the lead, have been instrumental in the very conception of China Mobile in 1997 and its subsequent expansion, thus helping the Chinese government consolidate and modernise the whole telecom sector. The study highlights the position of Hong Kong as an onshore-offshore financial centre intermediating between global financial markets and mainland China, and underwriting the reputation of China's ‘national champions’. The analysis also points to the advantages of Beijing over Shanghai as a command centre of state-owned and controlled enterprises, acting as a magnet for advanced business services. The relevance of global financial networks to China, a latecomer on the stage of financial globalisation, highlights the scope for applying the concept to the rest of the world, and its potential contribution to economic geography.

[93]

ZoroméA.2014.

Concept of offshore financial centers: In search of an operational definition

This paper offers additional evidence on the structure of the international financial network as emerging from the Coordinated Portfolio Investment Survey (CPIS) dataset collected by the IMF. Making use of blockmodeling techniques which allow us to fit a given community partition to real data, we show that the system is characterized by the presence of a particular type of meso-scale structure known as core–periphery, in which a densely connected subset of nodes (core) coexists with a sparsely connected partition (periphery), while the members of the core act as intermediaries between members of the periphery. The composition of the core – whose constituents are identified as the set of systemically important international financial centers – is rather small and remains stable over time. In addition to very large economies playing host to well-known global financial centers, the core comprises several off-shore financial markets.

... 随着人民币国际化的不断推进,人民币离岸中心成为一个热点.人民币离岸中心是指在中国境外经营人民币业务的自由交易、不受监管的国际金融市场,是人民币内外体系循环的节点.现有一些文献将构建香港人民币离岸金融中心作为研究对象进行分析(罗芳等, 2014),也有少数对中国其他地区建设人民币离岸金融中心的可行性进行探讨(陈丽英等, 2016),还有一些国外学者开始讨论其他国家的人民币离岸中心(Hall, 2017; Töpfer et al, 2017).哪些国家和地区会成为下一个人民币离岸中心将是一个非常有意义的议题,对中国人民币国际化的政策提出起到一定指导作用. ...

国际化背景下的香港人民币离岸金融中心建设

1

2014

... 随着人民币国际化的不断推进,人民币离岸中心成为一个热点.人民币离岸中心是指在中国境外经营人民币业务的自由交易、不受监管的国际金融市场,是人民币内外体系循环的节点.现有一些文献将构建香港人民币离岸金融中心作为研究对象进行分析(罗芳等, 2014),也有少数对中国其他地区建设人民币离岸金融中心的可行性进行探讨(陈丽英等, 2016),还有一些国外学者开始讨论其他国家的人民币离岸中心(Hall, 2017; Töpfer et al, 2017).哪些国家和地区会成为下一个人民币离岸中心将是一个非常有意义的议题,对中国人民币国际化的政策提出起到一定指导作用. ...

英属维尔京群岛离岸金融中心发展历程及启示

5

2017

... 注:根据孟广文等(2017)、许明朝等(2007)整理. ...

... 离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994).随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚.这种观点强调离岸金融中心是虚拟的、随机的.第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的.这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的.Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性.Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生.还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

... 从另一方面来说,当地政府或货币当局对其货币金融的管制加强或放松也是影响离岸金融中心产生的因素.第一种形式是对在岸政府监管加强的回应,Johns(1983)将政府干预市场的行为用“摩擦力”的概念来描述,离岸金融中心的环境比在岸市场更为宽松,因此存在很小甚至为零的“摩擦力”,也就推动了离岸金融中心的经营和发展.第二种形式是通过政策直接推动当地离岸金融中心的发展,这种离岸金融中心以发展离岸国际金融业务为主要特色,如开曼群岛、巴哈马、泽西岛等.另外,因为缺乏一些监管机构,“逃税”可能成“合理”的行为,一些法律还不是很健全的发展中国家更容易出现离岸金融中心,而且发展迅速(Clark et al, 2015).除此之外,国际政治经济环境、地理位置便利、政局稳定、自然灾害少、基础设施完善、金融法律服务专业、金融法律健全、政策优惠也是离岸金融中心形成的主要区位条件(杨叠涵等, 2013; 孟广文等, 2017). ...

... 事实证明,流向离岸金融中心的资金不一定总是流向监管最宽松的司法行政区,而是流向那些监管制度最有利于具体操作的司法行政区(Aalbers, 2017),而这个“利”往往涉及政治利益、经济利益和社会声誉等等,因此,今后的地理学对离岸金融中心的研究不仅要关注经济层面,更要与政治、社会学有交叉,这样才能帮助我们更好地理解离岸金融中心的起源、发展和未来趋势.除此之外,在全球化与金融化导致全球经济发展越来越不均衡的背景下,离岸金融业务和市场的内涵日趋复杂,离岸金融中心的空间格局可能会有所改变.由于传统离岸金融中心的衰落和新兴金融中心的崛起而重塑的新离岸金融格局以及背后的影响因素和作用机制都值得地理学再去探寻,同时也需要学者找寻新的视角来看待这些问题.对中国来说,在外商投资方面,自改革开放以来,以英属维尔京群岛、开曼群岛等为代表的避税港型离岸金融市场的对华投资额就一直保持前列(孟广文等, 2017),而大部分中国在海外上市的企业也选择这些离岸金融中心作为注册地(Pan et al, 2014),这种现象背后的原因以及中国如何融入全球离岸金融网络也值得地理学者思考. ...

英属维尔京群岛离岸金融中心发展历程及启示

5

2017

... 注:根据孟广文等(2017)、许明朝等(2007)整理. ...

... 离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994).随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚.这种观点强调离岸金融中心是虚拟的、随机的.第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的.这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的.Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性.Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生.还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

... 从另一方面来说,当地政府或货币当局对其货币金融的管制加强或放松也是影响离岸金融中心产生的因素.第一种形式是对在岸政府监管加强的回应,Johns(1983)将政府干预市场的行为用“摩擦力”的概念来描述,离岸金融中心的环境比在岸市场更为宽松,因此存在很小甚至为零的“摩擦力”,也就推动了离岸金融中心的经营和发展.第二种形式是通过政策直接推动当地离岸金融中心的发展,这种离岸金融中心以发展离岸国际金融业务为主要特色,如开曼群岛、巴哈马、泽西岛等.另外,因为缺乏一些监管机构,“逃税”可能成“合理”的行为,一些法律还不是很健全的发展中国家更容易出现离岸金融中心,而且发展迅速(Clark et al, 2015).除此之外,国际政治经济环境、地理位置便利、政局稳定、自然灾害少、基础设施完善、金融法律服务专业、金融法律健全、政策优惠也是离岸金融中心形成的主要区位条件(杨叠涵等, 2013; 孟广文等, 2017). ...

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

... 提到外国直接投资(Foreign Direct Investment, FDI),一般会想到实体投资,但实际上全球大约30%~50%的外国直接投资是通过离岸壳公司(Offshore Shell Companies)来实现的(Palan et al, 2014),壳公司是指实际金融业务均在母国进行的“空壳”,一些经济大国与某些避税港型离岸金融中心之间无需满足双重征税协议,且母国的金融机构可以享受该地区的优惠税收和宽松监管政策(郑强等, 2010).离岸外国直接投资的出现对传统的实体外国直接投资(Real FDI)是一个挑战.Haberly等(2015)利用全球FDI的数据构建出全球外国直接投资网络,发现离岸金融中心在全球FDI网络中的地位是中心而非外围的,这类投资的主要来源是英属维尔京群岛、卢森堡、开曼群岛、荷兰、瑞士和英国.在利用企业数据构建离岸外国直接投资的网络空间的研究中,Haberly等(2015)利用主成分分析法对全球离岸FDI网络进行分解,把全球分为“东部板块(Eastern Block)”“大英帝国(British Empire)”“大中国地区(Greater China)”和“美国和平协会(Pax Americana)”4个区域,证明全球离岸FDI是高度全球化的,但也集中在欧洲西北部和加勒比海地区的中心地带,并通过4个重要的历史事件解释了这些网络和子网络的形成. ...

加勒比海地区离岸金融业的发展与趋势分析

2

2010

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

... 提到外国直接投资(Foreign Direct Investment, FDI),一般会想到实体投资,但实际上全球大约30%~50%的外国直接投资是通过离岸壳公司(Offshore Shell Companies)来实现的(Palan et al, 2014),壳公司是指实际金融业务均在母国进行的“空壳”,一些经济大国与某些避税港型离岸金融中心之间无需满足双重征税协议,且母国的金融机构可以享受该地区的优惠税收和宽松监管政策(郑强等, 2010).离岸外国直接投资的出现对传统的实体外国直接投资(Real FDI)是一个挑战.Haberly等(2015)利用全球FDI的数据构建出全球外国直接投资网络,发现离岸金融中心在全球FDI网络中的地位是中心而非外围的,这类投资的主要来源是英属维尔京群岛、卢森堡、开曼群岛、荷兰、瑞士和英国.在利用企业数据构建离岸外国直接投资的网络空间的研究中,Haberly等(2015)利用主成分分析法对全球离岸FDI网络进行分解,把全球分为“东部板块(Eastern Block)”“大英帝国(British Empire)”“大中国地区(Greater China)”和“美国和平协会(Pax Americana)”4个区域,证明全球离岸FDI是高度全球化的,但也集中在欧洲西北部和加勒比海地区的中心地带,并通过4个重要的历史事件解释了这些网络和子网络的形成. ...

Financial geography I: Geographies of tax

1

2017

... 事实证明,流向离岸金融中心的资金不一定总是流向监管最宽松的司法行政区,而是流向那些监管制度最有利于具体操作的司法行政区(Aalbers, 2017),而这个“利”往往涉及政治利益、经济利益和社会声誉等等,因此,今后的地理学对离岸金融中心的研究不仅要关注经济层面,更要与政治、社会学有交叉,这样才能帮助我们更好地理解离岸金融中心的起源、发展和未来趋势.除此之外,在全球化与金融化导致全球经济发展越来越不均衡的背景下,离岸金融业务和市场的内涵日趋复杂,离岸金融中心的空间格局可能会有所改变.由于传统离岸金融中心的衰落和新兴金融中心的崛起而重塑的新离岸金融格局以及背后的影响因素和作用机制都值得地理学再去探寻,同时也需要学者找寻新的视角来看待这些问题.对中国来说,在外商投资方面,自改革开放以来,以英属维尔京群岛、开曼群岛等为代表的避税港型离岸金融市场的对华投资额就一直保持前列(孟广文等, 2017),而大部分中国在海外上市的企业也选择这些离岸金融中心作为注册地(Pan et al, 2014),这种现象背后的原因以及中国如何融入全球离岸金融网络也值得地理学者思考. ...

The offshore services industry in the Caribbean: A conceptual and sub-regional analysis

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

Editorial introduction to the special section: Deconstructing offshore finance

6

2015

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

... 离岸金融中心经常拿来与国际金融中心(International Financial Center, IFC)作比较,两者都处于全球金融体系的中心地位,是世界上最富裕的地方,因为它们运作着全球大部分的资金.一方面,这种相似性可能导致两者的竞争,国际金融中心虽然拥有健全的法律体系,却不能用低税率和保密法吸引到更多的企业和富人,于是一些国际金融中心也开始办理离岸业务,在岸(Onshore)和离岸的界限也越来越模糊,甚至还出现了一种所谓“中间岸”(Mid-shore)的行政区,例如中国香港和新加坡,它们综合了离岸的优势(低税率,保密)和一些在岸的特征(健全的法律体系、双边贸易协定、复杂的金融市场),一些在岸行政区甚至比离岸行政区拥有更加宽松的政策(Clark et al, 2015).如今,离岸中的“岸”已演化成为虚拟的岸,离岸金融的意义逐渐演变为制度性而非地域性. ...

Global finance and the growth of offshore financial centers: The Manx experience

3

1998

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

The financial secrecy index: Shedding new light on the geography of secrecy

2

2015

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

... 地理学者大约从20世纪90年代开始关注离岸金融中心,经过近30 a的研究,对离岸金融中心的认识逐步深化.早期的研究主要关注离岸金融中心的避税功能,后来开始关注保密等其他方面的功能(Hampton et al, 1999; Cobham et al, 2015),逐渐形成一个综合全面的视角.地理学的研究特色在于其独特的空间和网络视角:从微观尺度来说,每个离岸金融中心的地理位置、经济水平、殖民关系都不相同,这些地方特性能决定它们向不同方向发展;从宏观尺度来说,离岸金融中心只是全球金融体系中的一个组成部分,它们与其他组成部分之间会通过资金流动或社会关系而产生相互作用,把这些联系综合起来,也就形成了全球离岸金融的网络. ...

Integrating finance into global production networks

1

2014

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Geographical perspectives on mapping globalisation: An introduction to the JEG special issue mapping globalisation: Geographical perspectives on international trade and investment

1

2001

... 跨国公司与离岸金融中心的关系是通过离岸外国直接投资(offshore FDI)来实现的(Dicken, 2000, 2007; Coe et al, 2001; McCann, 2010).2008年金融危机之后,来自新兴市场的对外直接投资(Outward Foreign Direct Investment, OFDI)快速增长,对全球的金融地理格局产生了一定影响,而这些投资很大一部分是跨国公司的行为(Sharman, 2012).许多学者研究发现,由于两地税收差异带来的制度性套利是这种投资产生的主要原因(Lipsey, 2004). ...

Which countries become tax havens?

1

2016

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

Places and flows: Situating international investment

1

2000

... 跨国公司与离岸金融中心的关系是通过离岸外国直接投资(offshore FDI)来实现的(Dicken, 2000, 2007; Coe et al, 2001; McCann, 2010).2008年金融危机之后,来自新兴市场的对外直接投资(Outward Foreign Direct Investment, OFDI)快速增长,对全球的金融地理格局产生了一定影响,而这些投资很大一部分是跨国公司的行为(Sharman, 2012).许多学者研究发现,由于两地税收差异带来的制度性套利是这种投资产生的主要原因(Lipsey, 2004). ...

Global shift: Mapping the changing contours of the world economy

1

2007

... 跨国公司与离岸金融中心的关系是通过离岸外国直接投资(offshore FDI)来实现的(Dicken, 2000, 2007; Coe et al, 2001; McCann, 2010).2008年金融危机之后,来自新兴市场的对外直接投资(Outward Foreign Direct Investment, OFDI)快速增长,对全球的金融地理格局产生了一定影响,而这些投资很大一部分是跨国公司的行为(Sharman, 2012).许多学者研究发现,由于两地税收差异带来的制度性套利是这种投资产生的主要原因(Lipsey, 2004). ...

Tax havens: Renegade states in the international tax regime?

... 离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994).随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚.这种观点强调离岸金融中心是虚拟的、随机的.第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的.这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的.Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性.Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生.还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

... 离岸金融活动的实质就是资金在离岸金融中心与其他空间之间的流动,这些流动依靠跨国公司、富人和政府的对外投资来完成,而高阶商业服务(ABS)公司在这些个体产生相互作用的过程中起到了中介的作用.由于ABS公司拥有丰富的信息来源和专业技能,无论是跨国公司还是政府,都需要ABS公司的协助.跨国公司利用ABS公司来帮助他们筹集资金,了解外国法律法规和市场,而政府需要ABS公司来帮助他们制定合适的政策吸引跨国公司来此投资(Büthe et al, 2011).从人员构成来说,ABS公司也是金融精英、税务精英的集聚地,这些精英运用自身的专业知识和社会网络帮助企业和富人运转资金,并精心设计流程使得纳税义务最小化.Eden等(2005)提出,要理解离岸金融中心与在岸空间的互动关系,来自离岸金融中心的税务精英是一个很重要的切入点.Wainwright(2011)在英国住房抵押贷款证券化的研究中也发现,离岸金融的活动是一些金融专业人士群体和他们的客户通过紧密联系的社会网络架构而成,税务精英在投资网络中处于中心地位.他探究在信贷危机发生时,税务精英们如何利用立法漏洞使得“税务最小化”的策略得以实现,推动了英国经济金融化,但同时增加了信贷危机暴露的严重程度.Buckley等(2015) 以中国跨国公司为例,发现跨国公司是基于金融关系的网络,这些金融精英们的行为会影响资金的流动,从而对离岸金融中心和在岸空间的相互作用产生影响. ...

Lehman Brothers in the Dutch offshore financial centre: The role of shadow banking in increasing leverage and facilitating debt

1

2016

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

The world city hypothesis

1

1986

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

Uncovering offshore financial centers: Conduits and sinks in the global corporate ownership network

1

2017

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

Tax havens and the production of offshore FDI: An empirical analysis

Rethinking international financial centres through the politics of territory: Renminbi internationalisation in London's financial district

1

2017

... 随着人民币国际化的不断推进,人民币离岸中心成为一个热点.人民币离岸中心是指在中国境外经营人民币业务的自由交易、不受监管的国际金融市场,是人民币内外体系循环的节点.现有一些文献将构建香港人民币离岸金融中心作为研究对象进行分析(罗芳等, 2014),也有少数对中国其他地区建设人民币离岸金融中心的可行性进行探讨(陈丽英等, 2016),还有一些国外学者开始讨论其他国家的人民币离岸中心(Hall, 2017; Töpfer et al, 2017).哪些国家和地区会成为下一个人民币离岸中心将是一个非常有意义的议题,对中国人民币国际化的政策提出起到一定指导作用. ...

Treasure islands or fool's gold: Can and should small island economies copy Jersey?

1

1994

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Where currents meet: The offshore interface between corruption, offshore finance centres and economic development

... 地理学者大约从20世纪90年代开始关注离岸金融中心,经过近30 a的研究,对离岸金融中心的认识逐步深化.早期的研究主要关注离岸金融中心的避税功能,后来开始关注保密等其他方面的功能(Hampton et al, 1999; Cobham et al, 2015),逐渐形成一个综合全面的视角.地理学的研究特色在于其独特的空间和网络视角:从微观尺度来说,每个离岸金融中心的地理位置、经济水平、殖民关系都不相同,这些地方特性能决定它们向不同方向发展;从宏观尺度来说,离岸金融中心只是全球金融体系中的一个组成部分,它们与其他组成部分之间会通过资金流动或社会关系而产生相互作用,把这些联系综合起来,也就形成了全球离岸金融的网络. ...

Placing trust, trusting place: On the social construction of offshore financial centres

2

1998

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Offshore foreign direct investment, capital round-tripping, and corruption: Empirical analysis of Russian regions

2

2015

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

... 由于离岸金融中心在全球经济金融体系中的重要地位及其显著的区位特征,受到了地理学研究的广泛关注.离岸金融中心本身就有一个独特的地理视角,这些公司和个人作为发起方,因为税收、监管和保密等原因,注册和投资到母国之外的地方,加剧了资本在空间上的流动和集聚.分散来看,离岸金融中心只是一个个资本周转地,但综合所有的离岸金融中心可以让我们更好地了解现代金融体系网络化的运作模式(Lewis et al, 1987). ...

Geographies of money and finance II

1

1997

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Money order? The discursive construction of Bretton Woods and the making and breaking of regulatory space

1

1994

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Home-and host-country effects of foreign direct investment

1

2004

... 跨国公司与离岸金融中心的关系是通过离岸外国直接投资(offshore FDI)来实现的(Dicken, 2000, 2007; Coe et al, 2001; McCann, 2010).2008年金融危机之后,来自新兴市场的对外直接投资(Outward Foreign Direct Investment, OFDI)快速增长,对全球的金融地理格局产生了一定影响,而这些投资很大一部分是跨国公司的行为(Sharman, 2012).许多学者研究发现,由于两地税收差异带来的制度性套利是这种投资产生的主要原因(Lipsey, 2004). ...

The effectiveness of law, financial development, and economic growth in an economy of financial repression: Evidence from China

1

2009

... 相对发达国家来说,发展中国家更容易在离岸金融中心进行投资.有数据表明,发达国家在离岸金融中心的对外投资比例大约在25%~33%之间,而发展中国家如巴西、印度、中国等则基本在50%左右,2011年,中国甚至有74%的对外投资都在离岸金融中心(Palan et al, 2013).而众所周知,中国的经济不是完全由市场力量控制的(Vlcek, 2011; Karreman et al, 2012; Lai, 2012),“国有企业”(State Owned Enterprises, SOE)享有在体制内国有银行部门优惠的利率和优惠准入资本市场的特权(Naughton, 2007; Sutherland, 2009),相比之下,私营企业由于受到国家银行内部的贷款和国内股票市场的控制,在获得银行贷款方面面临重重困难 (Shen et al, 2009; Lai, 2011).因此,多数私人企业通常需要在中国以外寻找其他方法来增加他们的资本存量(Lu et al, 2009).Buckley等(2015)解释了中国企业在离岸金融中心注册的3种原因:第一,由于国内资本市场的不完善,对外投资者需要在他们的活动中寻求成本最小化的地点,于是选择在离岸金融中心注册(Buckley et al, 2007);第二,由于国内制度失调,中国企业可以利用一些专业机构,通过另一种相对优越的外国市场进行套利,最终使资金回流到国内,这种操作是“制度性套利”(Boisot et al, 2008);第三,中国企业在离岸金融中心注册是对国内税收制度变迁的反应,自2006年以来,新法规要求所有在海外投资的国民必须在当地的国家行政机关登记,还有政策限制境外控股公司注册的规定.因此,很多样本公司都明确表示将采取必要措施,减轻任何可能产生的不利影响①( http://www.sec.gov/Archives/edgar/data/1342068/000114420410023516/0001144204-10-023516-index.htm.),但事实证明,在减轻国内市场不完善的高成本方面,尽管去海外的成本增加了,收益仍然超过这些额外的成本,离岸金融中心仍然受到关注. ...

The geography of finance: Spatial dimensions of intermediary behavior

... 相对发达国家来说,发展中国家更容易在离岸金融中心进行投资.有数据表明,发达国家在离岸金融中心的对外投资比例大约在25%~33%之间,而发展中国家如巴西、印度、中国等则基本在50%左右,2011年,中国甚至有74%的对外投资都在离岸金融中心(Palan et al, 2013).而众所周知,中国的经济不是完全由市场力量控制的(Vlcek, 2011; Karreman et al, 2012; Lai, 2012),“国有企业”(State Owned Enterprises, SOE)享有在体制内国有银行部门优惠的利率和优惠准入资本市场的特权(Naughton, 2007; Sutherland, 2009),相比之下,私营企业由于受到国家银行内部的贷款和国内股票市场的控制,在获得银行贷款方面面临重重困难 (Shen et al, 2009; Lai, 2011).因此,多数私人企业通常需要在中国以外寻找其他方法来增加他们的资本存量(Lu et al, 2009).Buckley等(2015)解释了中国企业在离岸金融中心注册的3种原因:第一,由于国内资本市场的不完善,对外投资者需要在他们的活动中寻求成本最小化的地点,于是选择在离岸金融中心注册(Buckley et al, 2007);第二,由于国内制度失调,中国企业可以利用一些专业机构,通过另一种相对优越的外国市场进行套利,最终使资金回流到国内,这种操作是“制度性套利”(Boisot et al, 2008);第三,中国企业在离岸金融中心注册是对国内税收制度变迁的反应,自2006年以来,新法规要求所有在海外投资的国民必须在当地的国家行政机关登记,还有政策限制境外控股公司注册的规定.因此,很多样本公司都明确表示将采取必要措施,减轻任何可能产生的不利影响①( http://www.sec.gov/Archives/edgar/data/1342068/000114420410023516/0001144204-10-023516-index.htm.),但事实证明,在减轻国内市场不完善的高成本方面,尽管去海外的成本增加了,收益仍然超过这些额外的成本,离岸金融中心仍然受到关注. ...

Elsewhere, ideally nowhere: Shadow banking and offshore finance

5

2014

... 离岸金融(Offshore Finance)是现代金融业演进中最重大的创新之一,在全球金融体系中占据越来越重要的地位.2010年IMF调查数据显示,离岸金融中心(Offshore Financial Center, OFC)的资产已经超过一些发达国家的经济总量,如法国、德国和日本(郑强等, 2010).不仅如此,它们还是全球金融网络中跨国资本存储和重新分配的节点,在全球与区域产业分工和发展中发挥着重要的作用(Clark et al, 2015).据估计,英美前100大上市公司中至少有80%在离岸金融中心设立了分支机构,而世界50%的跨境资产和负债通过离岸金融中心进行转移(Palan et al, 2014; Garcia-Bernardo et al, 2017),越来越多的企业、个人和其他中介机构选择离岸金融中心作为金融活动的场所.金融学家把离岸金融中心称作大型经济体之间的“金融接口”和“连接全球金融的媒介”,他们认为全球化导致贫富差距不断扩大,而离岸金融中心是全球化过程中的核心要素(Chavagneux et al, 2010). ...

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

... 离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994).随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚.这种观点强调离岸金融中心是虚拟的、随机的.第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的.这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的.Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性.Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生.还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

... ; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

... 提到外国直接投资(Foreign Direct Investment, FDI),一般会想到实体投资,但实际上全球大约30%~50%的外国直接投资是通过离岸壳公司(Offshore Shell Companies)来实现的(Palan et al, 2014),壳公司是指实际金融业务均在母国进行的“空壳”,一些经济大国与某些避税港型离岸金融中心之间无需满足双重征税协议,且母国的金融机构可以享受该地区的优惠税收和宽松监管政策(郑强等, 2010).离岸外国直接投资的出现对传统的实体外国直接投资(Real FDI)是一个挑战.Haberly等(2015)利用全球FDI的数据构建出全球外国直接投资网络,发现离岸金融中心在全球FDI网络中的地位是中心而非外围的,这类投资的主要来源是英属维尔京群岛、卢森堡、开曼群岛、荷兰、瑞士和英国.在利用企业数据构建离岸外国直接投资的网络空间的研究中,Haberly等(2015)利用主成分分析法对全球离岸FDI网络进行分解,把全球分为“东部板块(Eastern Block)”“大英帝国(British Empire)”“大中国地区(Greater China)”和“美国和平协会(Pax Americana)”4个区域,证明全球离岸FDI是高度全球化的,但也集中在欧洲西北部和加勒比海地区的中心地带,并通过4个重要的历史事件解释了这些网络和子网络的形成. ...

Going global? Examining the geography of Chinese firms' overseas listings on international stock exchanges

1

2014

... 事实证明,流向离岸金融中心的资金不一定总是流向监管最宽松的司法行政区,而是流向那些监管制度最有利于具体操作的司法行政区(Aalbers, 2017),而这个“利”往往涉及政治利益、经济利益和社会声誉等等,因此,今后的地理学对离岸金融中心的研究不仅要关注经济层面,更要与政治、社会学有交叉,这样才能帮助我们更好地理解离岸金融中心的起源、发展和未来趋势.除此之外,在全球化与金融化导致全球经济发展越来越不均衡的背景下,离岸金融业务和市场的内涵日趋复杂,离岸金融中心的空间格局可能会有所改变.由于传统离岸金融中心的衰落和新兴金融中心的崛起而重塑的新离岸金融格局以及背后的影响因素和作用机制都值得地理学再去探寻,同时也需要学者找寻新的视角来看待这些问题.对中国来说,在外商投资方面,自改革开放以来,以英属维尔京群岛、开曼群岛等为代表的避税港型离岸金融市场的对华投资额就一直保持前列(孟广文等, 2017),而大部分中国在海外上市的企业也选择这些离岸金融中心作为注册地(Pan et al, 2014),这种现象背后的原因以及中国如何融入全球离岸金融网络也值得地理学者思考. ...

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

The preeminence of international financial centers

1

1981

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

From double tax avoidance to tax competition: Explaining the institutional trajectory of international tax governance

1

2011

... Wójcik(2013b)指出,“如同全球城市一样,不能简单地回答一个行政区是否是离岸金融中心,它是一个程度问题”.因此,本文把离岸金融定义为在高度自由化和国际化的金融监管体制下,在一国金融体系之外、由非居民参与的资金融通的市场,就是离岸金融市场,市场所在地就是离岸金融中心.离岸金融中心有以下几个特征:第一,非居民性,即参与离岸金融业务的存款人和借款人均为中介机构所在国或地区的非居民,也就是通常所说的“两头在外”.第二,这些金融资本仅仅在离岸金融中心范围内流通,是“资金中转站”,不包括实体的对内投资:一方面,它们是上市企业的注册地和各类壳公司的所在地,许多跨国公司和配套的服务企业来此投资,将全球大量的资金集聚在一起;另一方面,ABS公司运用特定的金融工具来完成资金的流转,使得资金又重新分配到世界各地,离岸金融中心也是跨国投资的来源地(Rixen, 2011; Sayer, 2015).第三,离岸金融中心有特殊的制度安排,主要包括:①离岸金融中心是一个相对自主的司法行政区,可以不受国家或政治组织的管理限制,经营运作非常灵活;②优惠的税收结构,许多经济学家将离岸金融中心称作“避税天堂”,可见离岸金融中心的基本功能就是帮助企业和富人避税,它们通过使用信托、咨询公司或者其他经济实体,对资金流动路径进行规划和管理来使纳税人义务最小化(Booijink et al, 2007);③保密性较高,尤其是一些簿记中心(资金来源和运用都在境外的离岸金融中心).除此之外,离岸金融中心的特征往往还包括拥有优越的地理位置、稳定的政治经济环境、金融体系完善程度高、基础设施条件齐全以及国际声誉良好等. ...

Why reregulation after the crisis is feeble: Shadow banking, offshore financial centers, and jurisdictional competition

1

2013

... 过去30 a间,新兴金融市场得到了极大发展,其中离岸金融中心的形成和发展加快了全球金融一体化的步伐,同时也改变了国际金融中心的竞争格局.一般来说,处于国际金融体系核心地位的是全球顶级的金融中心,如伦敦、纽约和东京,它们凭借巨大的资本量加速资本的流动(Reed, 1981; Sassen, 2001),然而,对于一些低于全球平均水平的金融中心,等级与资本量的联系似乎不那么清晰(Friedmann, 1986),反而是分散在世界边缘地区且处于较低层级的小型金融中心,如马恩岛、开曼群岛、泽西岛等在世界经济体系中愈发得到重视.早期的离岸金融中心通常是一些很小的岛屿,基本上人口不到100万(Dharmapala et al, 2006),但却拥有低廉的税金、稳定的政治环境和保密的法律,能帮助企业和个人避 免或减轻税务负担(Hudson, 1999).也正因为如此,它们经常被贴上“洗钱、犯罪、贪污腐败”的标签(Quirk, 1997).事实上,离岸金融中心确实在金融危机中发挥了一些作用,亚马逊、苹果、谷歌这些大公司的丑闻往往也与离岸金融中心有关 (Rixen, 2013; Palan et al, 2014; Seabrooke et al, 2014; Fernandez et al, 2016). ...

Fictitious capital, fictitious spaces: The geography of offshore financial flows

3

1994

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

... 离岸金融中心目前已经实现全球化布局,那么这些国家和地区是随机产生的还是“必然”的呢?20世纪90年代,经济地理学领域存在2种观点:第一种观点认为离岸金融中心是“可替代的”,会因为制度的改变不断面临被取代的风险(Roberts, 1994).随着通信技术的发展,距离的限制被消除,但因为面对面交流在金融活动中仍然是相当重要的,因此,在相近的时区,一些离岸金融中心会形成一种纵向的集聚.这种观点强调离岸金融中心是虚拟的、随机的.第二种观点认为离岸金融中心基于深厚的历史和社会根源,是当地的政治、历史事件、殖民文化等造成的.这种观点与离岸金融中心是随机选择的地点不同,主张离岸金融有一个惯性,是基于当时的时代背景或当地的社会历史联系而形成的,因此离岸金融中心的地点是相对“稳定”的.Warf(2002)将巴拿马成为拉丁美洲最重要的国际银行中心的原因归结为运河遗产、长期以来禁止反对黄铜板银行(Brass Plate Banking)、早期的美元化经济和免税殖民贸易区4个历史事件的作用,认为这种独特的历史地理和制度性改变是巴拿马和其他竞争者与众不同的地方,强调了历史和社会因素的重要性.Palan等(2014)认为英国和他们的殖民者因为有共同的法律和文字而促进了离岸金融活动的产生.还有一些研究表明离岸金融中心的发展与当时欧洲贵族的家庭网络和英国殖民的遗留遗产有关(Eden et al, 2005; Palan et al, 2014).Wójcik(2013a)提出了“纽伦轴线(New York-London Axis, NY-LON Axis)”的概念,指出这不仅是2个领先的全球城市,还是2个最重要的离岸金融中心,它们掌握全球40%的离岸金融活动.他指出,离岸和在岸的金融服务在这2个城市间不断加强,是因为伦敦金融区(the City of London)和纽约存在着殖民关系,维持这2个离岸金融中心的共同发展.孟广文等(2017)对英属维尔京群岛离岸金融中心发展与空间集聚影响因素进行研究,也认为独特的人文经济因素为离岸金融市场的建立提供了基础.由此可见,更多的学者认为离岸金融中心是“固定”的,相比于地理位置来说,社会历史条件更能促进一个地区发展成为离岸金融中心. ...

Small place, big money: The Cayman Islands and the international financial system

1

1995

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...

Offshore financial centres: Parasites or symbionts?

A phantom state? The de-traditionalization of money, the international financial system and international financial centres

1

1994

... 地理学者从20世纪90年代开始关注这方面的问题.较早关注到离岸金融中心的经济地理学家是Roberts(1994, 1995),他指出虽然离岸金融中心往往都很小,但却是反映国际资本流动的窗口,并认为只有从空间和距离的角度进行研究,才能理解离岸金融中心的形成和国际金融市场的变化.随后开始出现更多关于离岸金融中心的地理学研究,主要关注那些拥有相对宽松金融市场和保密法的小岛,且这些研究多采用案例分析,如Hampton(1994)研究泽西岛(Jersey);Cobb(1998)研究马恩岛(Manx);Hudson(1998)研究巴哈马群岛和开曼群岛(the Bahamas and the Cayman Islands),他们用社会学或政治学的理论建构出不同的分析框架,揭示离岸金融中心在全球金融体系中的地位.但当时大多数研究还是集中在世界上主要的国际金融中心和主流金融市场,因此有关离岸金融的理论研究还在萌芽阶段,实证研究也很缺乏(Leyshon et al, 1994; Thrift et al, 1994; Leyshon, 1997).近年来,地理学界突破了过去对单一离岸金融中心案例分析的局限,开始从更大的尺度进行分析,研究离岸金融中心和全球金融体系中其他组成部分的互动关系和全球离岸金融网络(Cobham et al, 2015; Ledyaeva et al, 2015).在这类研究中,全球金融网络(Global Financial Network, GFN)成为重要的视角.全球金融网络(GFN)的概念来源于全球生产网络(Global Production Network, GPN),Coe等(2014)认为,金融业较制造业而言更加全球化与网络化,于是他们从金融地理与相关文献中,萃取出“全球金融网络”(GFN)的概念,提出网络的3个核心要素是高阶商业服务(Advanced Business Services, ABS)、世界城市(World Cities, WCs)和离岸行政区(Offshore Jurisdiction, OJ).离岸行政区即离岸金融中心的别称,把离岸金融中心放入全球金融网络中进行研究,不仅能理解离岸金融中心本身,还能理解它们与全球金融体系中其他组成部分的互动关系. ...